April 17, 2026

Stephan Colavito, President and CIO, Zofingen Private Wealth, LLC.

ZPW Insights are made available to Cenerus customers through an ongoing collaboration.

For more information or to schedule a briefing contact your Cenerus representative or visit www.ZofingenPWM.com.

Nikola Tesla was a Serbian American engineer, futurist, and inventor. He is known for his contributions to the design of the modern alternating current electricity supply system (aka: AC/DC – not the rock band!).

Tesla was ahead of his time with his work in mechanical oscillators/generators, electrical discharge tubes, and early X-ray imaging. He also built a wirelessly controlled boat, one of the first wireless-controlled vehicles ever produced. Tesla became well known as an inventor and demonstrated his achievements to celebrities and wealthy patrons at his lab. Known as “showman,” his pursuit of wireless lighting and worldwide wireless electric power distribution in his high-voltage, high-frequency power experiments. Tesla tried to put these ideas into practice in his unfinished Wardenclyffe Tower project, an intercontinental wireless communication and power transmitter, but ran out of funding before he could complete it.

We could spend a whole blog post on all the accomplishments and inventions attributed to Nikola Tesla. There is a reason why one of our greatest modern-day inventors (Elon Musk – politics aside) named his electric car company after Tesla. What is interesting is that Tesla died shortly after being hit by a taxicab (ironic, wouldn’t you say) in New York, which caused broken ribs and a massive back injury. Nikola never recovered and died at the age of 86 alone in room number 3327 of the New Yorker Hotel with no money and enormous debt.

This week, we are going to focus on all sorts of power. We are playing a little AC/DC while writing this week, and we hope you are “Thunderstruck” by the data we present. Let the betting begin on the under/over on the puns this week.

The Power of Momentum

A few weeks ago, in our “Shock and Awe” post, we stated, “There is some good news if/when this war ends. We anticipate the equity and bond markets rallying as they breathe a sigh of relief and can contain their ‘deeper tail’ scenarios (which exist today). Those will get priced out of the market when it’s over, and we expect a potential appreciation in the 5-10% range.”

Well, we were wrong. It didn’t take the war ending to get a rally; it took the beginnings of the war ending for FOMO traders to jump back in and rally the market higher (the Dow is up over 800 points today on comments from President Trump on the opening of the Strait). Momentum is clearly in control at the moment, as nothing seems to matter. Oil, volatility, and macroeconomic conditions are all being ignored as mechanical buying keeps pushing markets higher.

There were plenty of hedge funds that were short the market before this rally, only to see their “faces ripped off” as markets have headed higher. The short squeeze in the Magnificent Seven is a great example. Since breaking above the negative trend line (outlined below), these stocks have exploded higher. The violent move higher is in part due to dip buyers and another part to short covering (source: first two charts, Market Ear).

Despite equities remaining largely impervious to global macro concerns at the headline level, weak breadth (stocks advancing versus declining in the market index) and a messy narrative continue to give us concerns. We believe the setup is more fragile than the media (CNBC) is disclosing. We would need to see earnings hold above expectations and oil to stabilize below $85 before we feel comfortable adding additional equity exposure.

Oil Power

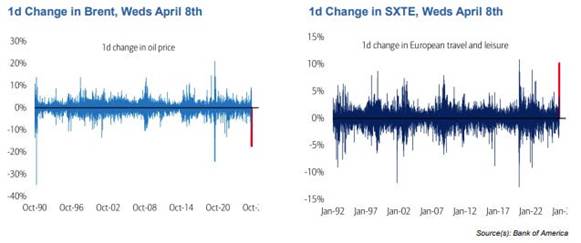

With the ceasefire announcement, the market saw the largest intra-day drop in Brent crude prices since the Gulf War in 1991 and the largest intra-day move higher in European Travel and Leisure equities since 1992, other than the announcement of a COVID vaccine in November of 2022. This highlights the market’s skittishness, as investors are just as concerned about missing the rally as about a potential sell-off.

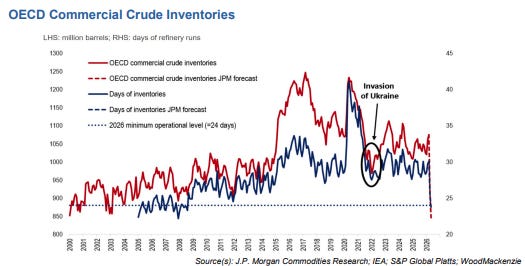

However, despite the relief rally in crude, the world is approaching what is referred to as the “operational minimum,” the floor below which the global oil system begins to lose functionality. The OECD commercial crude inventories have already fallen to roughly 968 million barrels, which is equivalent to just 27 days of forward refining demand. The effective loss of 14 mbd from the closure and now blockade of Hormuz is so large that the market is focused on inventory draw and demand destruction (read our blog called “Shock and Awe” on what demand destruction does to global economies).

In this context, some estimate that OECD commercial crude inventories will draw down by roughly 166 million barrels in April and a further 67 million barrels in early May, before hitting the operational minimum of 842 million barrels. To put this in terms we all understand (unless we drive a Tesla), it is like seeing that little gas tank light on your dashboard when you are close to empty.

This week, the Head of the European Energy Agency warned that Europe has “maybe six weeks or so” of remaining jet fuel supplies, and that the agency expects widespread cancellation of flights without additional jet fuel.

The lack of supply is hurting not just Europe, but poorer countries in Asia, Africa, and Latin America.

Alternating Current

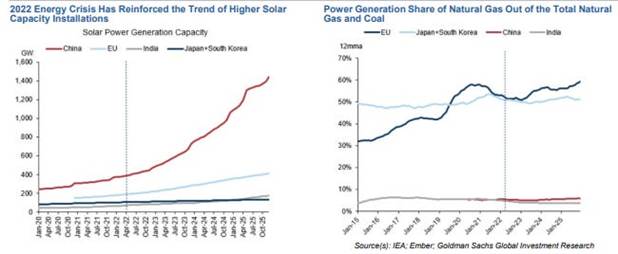

The Middle East conflict further incentivizes economies to prioritize the security of energy supply by moving toward more localized sources. In contrast to developed and leading emerging economies, coal has gained share from natural gas in power generation in South and Southeast Asian countries, such as Bangladesh, Pakistan, and Vietnam, which are opening coal plants. Lacking rapid renewable ramp-ups, these countries have prioritized energy security, which remains more affordable and accessible via domestic production or regional trade.

As emerging markets move to coal (cheap and easy to convert to energy), we anticipate developed countries (except the United States under the current administration) will continue to move towards wind and solar. As we have noted since the war began, many refineries in the Middle East have been damaged. As a result, even as the Strait of Hormuz was said to be opened today, it would take considerable time to restore oil flows to pre-war levels.

As many observers have highlighted, there is an unusually large disconnect between spot (physical) oil prices and underlying futures (future supply and price). Currently, Brent crude is down to around $90.03 per barrel versus June futures at $101. With the last deliveries from the Gulf (shipped before the war) arriving in many jurisdictions this coming week, inventories will be drawn down at an accelerated pace, and in turn, place much more upward pressure on prices across the oil curve.

Like alternating current itself, energy markets keep whipsawing directions, and the reversals are making it hard for countries and investors to adapt.

Purchasing Power

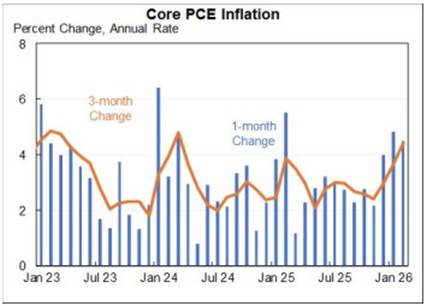

Core PCE inflation, which is the Fed’s favored target, came in at 3.0% year-over-year in February before the current energy price shock. Further, core goods inflation rose 0.8% in February. More dovish Fed officials had expected core goods inflation to no longer impact year-over-year rates by around Q2 or Q3 2026. That now seems to have changed, with the Fed pushing it back to early 2027 as it positions for a little more hawkishness, given the slim-to-none prospects of getting inflation to its target rate of 2%.

Projections for March suggest a continued rise with core PCE estimated to rise by 0.3% and year-over-year reaching close to 4%.

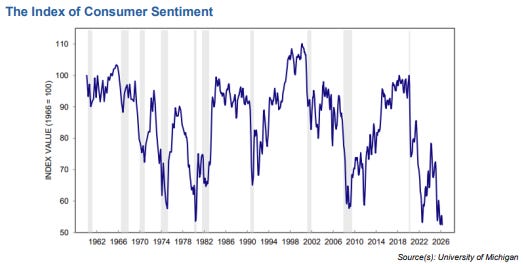

In simple terms, four consecutive price shocks in five years (COVID, Russia vs. Ukraine, Tariffs, and now Iran/Oil) have broken the American Consumer’s confidence in a way no single data point fully captures until now. This month’s Michigan Survey posted its lowest level EVER since the launch in 1951. The Survey’s authors note, “Demographic groups across age, income, and political party all posted setbacks in sentiment, as did every component of the index, reflecting the widespread nature of this month’s fall.”

Even before the war and the resulting higher gas prices, we had highlighted that US consumers were stressed. One of the data points we look at is the BNPL (buy now pay later) delinquency rates.

BNPL is now the fastest-growing delinquency problem in consumer lending, with rates surging from 34.0% to 42% of all loans in two years. Think about that, over 40% of the BNPL loans are not current. With almost 350 million people in the US, a third are using BNPL services, and a global debt market of 560 billion dollars in loans.

The trajectory of consumer delinquencies in this space is eye-opening:

· 2023: 34% of all loans had at least one late payment

· 2024: 39% of all loans had at least one late payment

· 2025: 42% of all loans had at least one late payment.

Looking at the chart above, it’s clear that consumers still want to spend, with a large number of consumers using BNPL platforms to buy things (including groceries). Currently, the average write-off for the BNPL loans is just under 5%. We expect delinquencies to rise by an additional 2% over the next 12 months.

Grounded

Over the last few weeks, we have been questioned by clients about selling positions and moving to cash. Given the uncertainty, many people are nervous. It’s a crazy time. But we are never smart enough to time the market, and always suggest holding good fundamental positions (we are investors, not traders).

However, we would be more aggressive in reducing exposure if we started to see signs of the economy falling into a recession or even worse, stagflation. Equities do not perform well in these economic cycles, and they typically take considerable time to return to a growing GDP.

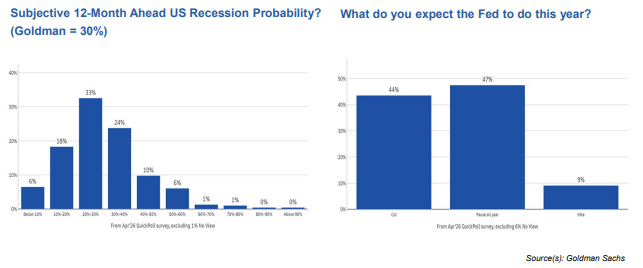

Polymarket has recession odds of 29% by the end of the year, while Goldman Sachs has raised its probability to 30% over the next 12 months. In a poll of investors conducted by Goldman, most investors were in the 20-40% probability group for a recession, while most also believed growth would be between 1.5% and 2.5% (Goldman’s estimate is 2.3%). In the same survey, they found that very few believed the Fed would hike this year, while 44% believed they would cut. Currently, market pricing is for no hikes or cuts this year (we have one cut on our BINGO card for 2026).

Survey participants estimate that core inflation would be between 2.5% and 3.5% at the end of this year (GS estimates 2.9%, while our estimate is 3.1%). This all highlights the difficult task ahead for the Fed with persistently elevated core inflation and a very wide distribution of growth expectations.

After the latest “Truth Social” post, systematic buying is running at one of the fastest paces on record. Over $86 billion in global equities have been bought over the last five weeks, the highest total in the top five all-time. Goldman Sachs believes another $70 billion will enter markets in the next few weeks.

If history repeats, this type of equity-buying burst tends to lead to short-term consolidation and/or a pullback. This market is feeling a bit much. But longer-term history suggests equities move higher. This is why we say we are not “Tesla smart” to time the market.

Power without distribution is just potential energy

Equity markets are driven by momentum. For all of Tesla’s brilliance in understanding power, he could never control who distributed it. It is our job to be pragmatic and realize how to harness markets and data for our benefit.

Risk assets can continue to trade well now that we are past peak stress, with the market again focusing on earnings and growth expectations. We would like to see a consolidation, but we don’t have control over that. We are not chasing markets here, but will continue to watch and wait with new money. For bonds, we think the front-end part of the range (1-5 years of maturities) should trade in a range.

Our eyes are now on private credit, economic growth, inflation, and labor markets. We use data to make informed investments so we can continue to be “Back in Black” with our clients’ accounts.

As a parent of a Marine, we are thankful this war seems to be coming to an end.

Have a great week.

For more on Zofingen Private Wealth go to www.ZofingenPWM.com

General Disclosures

This research is for ZPW and Cenerus clients only. The opinions represented in this research are those of the President/CIO, not advisors or officers of ZPW, Cenerus, or San Blas Securities. This research is based on current public information that we consider reliable; however, we cannot guarantee its accuracy or completeness, and it should not be relied upon. The information, opinions, estimates, and forecasts contained herein are as of the date hereof and are subject to change without prior notification. We seek to update our research as appropriate. Some research can and will be published irregularly as applicable in the analyst’s judgment.

This research is not an offer to sell or solicitation of an offer to buy a security in any jurisdiction where such an offer or solicitation would be illegal. It does not constitute a personal recommendation or take into account our clients’ particular investment objectives, financial situations, or needs (individual or corporate). Clients should consider whether any advice or guidance in this research suits their specific circumstances and, if appropriate, seek professional advice, including tax advice. Past performance is not a guide for future performance, future returns are not guaranteed, and a loss of original capital may occur. More information on Zofingen Private Wealth is available at www.zofingenpwm.com and Cenerus at www.cenerus.com.